Looking For a Financial Advisor for MedTech Professionals?

Are you a professional working in the MedTech industry? A financial advisor who understands the unique needs of MedTech careers such as medical device representatives, executives, and founders in this industry can help you make smarter money moves throughout your career.

Achieving success in the fast-paced world of medical devices involves more than just knowing your products or being a great salesman. Among the non-stop workdays that are filled with appointments and high-stakes conversations, one important thing often gets forgotten: financial planning. To avoid adding even further stress to their daily routine, MedTech professionals stand to benefit from the expert guidance of a financial advisor who understands their unique circumstances.

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it may be more difficult to find a financial advisor who specializes in serving MedTech professionals. That’s where we come in!

Financial Planning for MedTech Professionals

Matt Nelson, CFP®, AIF®, ECA

Founder and Managing Partner of Perspective 6 Group, specializing in helping Medical Technology industry professionals eliminate their financial stress and plan for financial freedom.

Q & A: Financial Advisor Specializing in Serving MedTech Professionals

Answer:

Having sufficient time and energy to step away from saving the world to plan for themselves and their families.

Executives in this industry are especially busy, with constant complex decision points to make. They are mission-driven professionals who focus on the impact they can make through their careers. However, their careers don’t allow the time or energy to focus on keeping their own financial house in order.

These professionals typically have high-income and complex benefits that include equity compensation and deferred compensation plans. While many work in large publicly traded companies, a significant portion of the industry consists of small to medium-sized start-ups and private companies. This creates unique risks and rewards when evaluating job offers and leaving established companies, salaries, and benefits behind.

Further, medical device sales reps typically earn high incomes with much variability depending on bonus or commission plans. Further, they’re often faced with equity compensation decisions. For example, whether to take less base pay or variable pay in lieu of more stock compensation.

Individuals in these roles often feel under pressure or high stress. An advisor who understands their situation, company, and industry so they can delegate the details puts their mind at rest.

Answer:

The question of whether to hire an advisor and when has become increasingly common. Information and data seem easy to find with tech advances and internet searches. And now with AI it can initially seem advice providers are becoming irrelevant.

However, having all the data available to you is not the same as understanding what to do with it. Think about your own industry and how it interacts with healthcare providers. Without people in place helping patients decide when to use the produce the breakthrough medical device your company created isn’t any good. Further, the device requires someone knowledgeable who can interpret the results and make course corrections.

So, when beginning to consider hiring a financial advisor, think about why you seek help in other areas of life. When would you hire a doctor? A lawyer? Do you prepare and file your own taxes? Much of the information needed to handle these areas of your life can be found on the internet as well. Still sorting through the options and decision matrixes can be daunting. It is better to spend time furthering your career or with family and pay someone else to do it. With the added benefit of the work getting done quicker with higher quality than what your capacity allows.

Here are examples of questions that professionals in MedTech face where a financial advisor can offer expert guidance:

- Do you participate in any equity compensation plans?

- Is your employer a private company with a plan to go public or be acquired in the future?

- Are you earning above $200k/single or $385k/married (pushing into the 32%+ tax bracket) and facing additional tax planning complexity?

- Do you own multiple real estate properties or plan to in the future?

- Are you within five years of retirement or planned independence?

- Are you considering leaving a long-time position at a publicly traded company to start your own company?

Answer:

Our firm provides a niche offering to the MedTech and MedDevice industry. This focus allows us to understand career tracks and benefit plans better than generalist advisors. We know the complex environment executives and managers face and how it might affect their own planning.

Point #1: Sales Reps

We understand the unique career challenges of MedDevice sales with its high variable compensation and job mobility. These positions can be dependent on startup company funding and at risk of job losses outside their control. Making it difficult to balance a long-term saving plan with the need for short-term emergency cash. Further, many reps often feel like they can’t trust how long personal success will last. Resulting in a hesitancy to tie up capital and subsequently too much cash on hand and not enough long-term investments. Our team works with reps to meet immediate needs as well as future, so they can retire well.

Point #2: Benefits & Equity Compensation

We know the complex benefit plans of the industry’s large, publicly traded companies. We provide guidance on how to maximize those benefits to plan for the future you envision. As well as considerations when moving jobs to startups or private companies.

Point #3: Entrepreneurs & Start-Ups

Company founders and start-up entrepreneurs in this industry often face outsized risk. Many starting later in life with more to lose. The mission-driven nature of this work means founders can be vulnerable. Putting too much time, energy, and financial resources into their company than might be prudent. Our team acknowledges those circumstances and ensures they are well-advised. We prepare and advocate for founders from launch and beyond to protect the wealth they accumulate.

Point #4: Retirement Planning

In retirement planning in MedTech we know the potential pain points. Our team can account for a career with significant equity compensation and the concentrated stock risks faced because of it.

See What We Can Do For You

The first step is a quick conversation to see if we can help.

Our calls are always relaxed and pressure-free.

Answer:

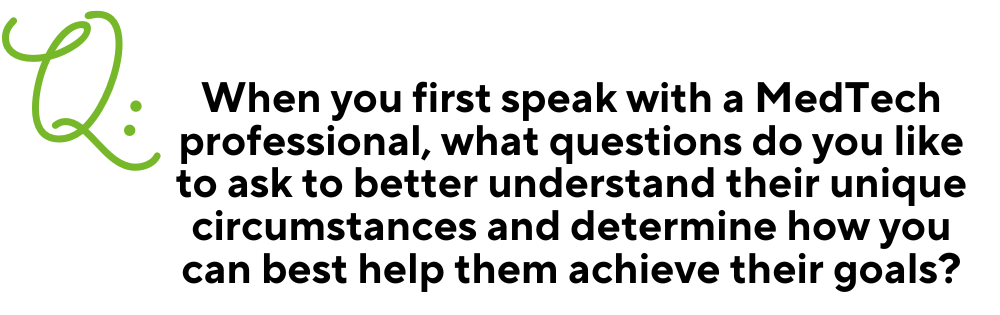

When meeting for the first time, we look to understand what is motivating someone to seek help from an advisor. Are we dealing with a referring symptom or the primary pain point? For instance, is there a tax concern driven by recently receiving stock compensation for the first time in a job? Or is there the larger question of how to plan for retirement and whether those goals are on target? Of the many questions we might ask, some of the key ones are:

- What specifically is on your mind that caused you to reach out today?

- What is most important to you?

- What does money mean to you?

- Do you see yourself in your current career and company for more than 5 years? More than 10?

- Do you receive significant income from equity compensation?

- What strategies are you using to optimize your taxes?

- Do you often owe large amounts or receive large refunds at tax time?

- What financially related plans do you have for family and other important relationships in your life?

- Are you the primary income earner in the family?

- Do you have dreams of starting your own company or joining a start-up?

- At what age do you want to be financially independent? Do you hope to retire early?

Answer:

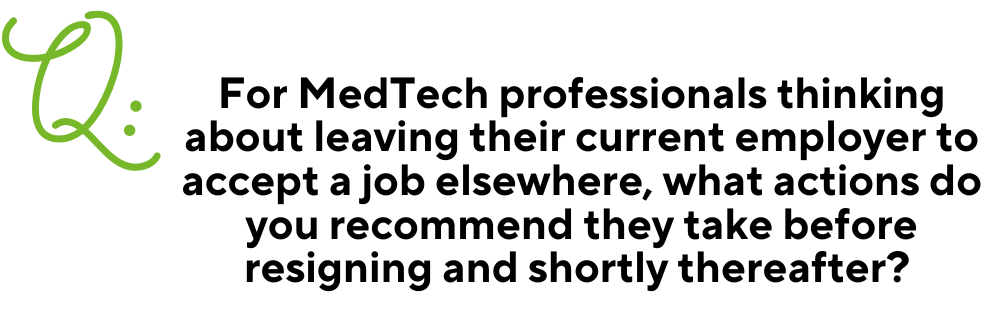

Thoroughly review and understand your vesting schedules. 401(k) plan company contributions often have a graded or even cliff vesting period. These could result in giving up significant benefits if you are leaving early. The same can be said for equity compensation instruments. Make sure you understand what you can keep and how long you’ll have to capture their value. Then make a plan to capture any vested stock options before leaving or within the required time limit post termination. If no plan is in place, there is the risk of losing all value.

Be aware of key dates of employment to achieve in a given calendar or fiscal year. These are set as markers to receive company plan contributions, bonus pay, or equity incentives. Leaving prior to these dates, which may all be different, can be an unintended but still unfortunate mistake.

Understand your insurance plan continuation options. Will your medical insurance be maintained continuously as you transition? What will happen to the life insurance your family is relying on? Will the new company offer equivalent benefits, or will you need to obtain coverage on the private market? Which will require more extensive medical underwriting?

Finally, make sense of the job offer – particularly with equity compensation. In a public company, it is easy to calculate the value of RSUs and stock options. Knowledge of the vesting requirements and volatility of the stock price is equally as important. Especially, considering you are trading base compensation for them. In private companies it is difficult to understand the value of equity being offered and whether it will materialize. Do not get caught up with offers of large numbers of equity units that technically are not worth anything yet. You may not even be around long enough to realize their value.

Answer:

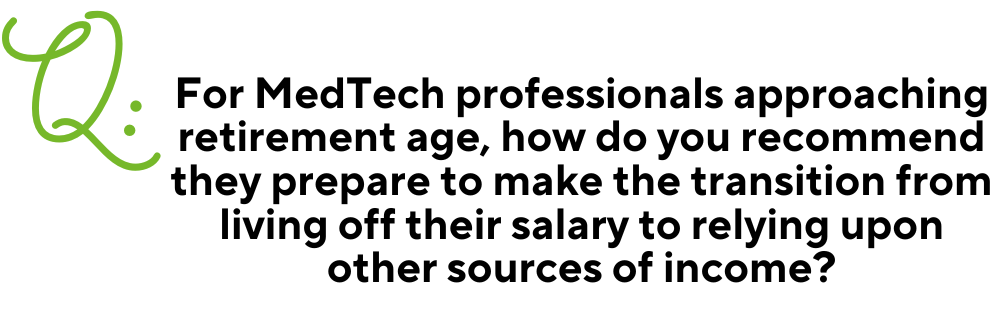

Know your goals and how to utilize your resources to achieve them. Begin by creating a plan that illustrates and organizes all the various income and cashflow sources you’ll have. Consider their tax ramifications and whether they’ll continue past your lifetime to those you care about. Find a financial advisor who can guide you through every step and nuance MedTech careers create.

The concentrated company stock that you have accumulated over many years may be a core accumulation vehicle with great returns. However, as you transition, and it becomes necessary to retirement income it could add significant risk.

Begin to diminish risk in your financial portfolio by moving out of company stock and any other concentrated positions. Do this in as tax-efficient a way as possible, even if this is a multi-year process. The proceeds from these sells should fund a more diverse portfolio that will support your retirement lifestyle. Our team of specialized retirement planners is available to guide you in this process seamlessly.

Further, have a plan for RSUs, stock options, and deferred compensation plans. These will need wrapping up along with conversion to an income portfolio. While restricted stock plans may be straightforward, deferred compensation plans are not. Those will need careful coordination with other forms of income to minimize taxes owed over a multi-year span.

Transition to retiree medical insurance, whether through the company’s retirement benefit or a personally owned policy. You’ll need to have coverage that will bridge to Medicare age if you are retiring before age 65. Also, consider whether now is the time to add long-term care insurance. While it seems like years away, these insurance policies are much cheaper to add at a younger age.

Answer:

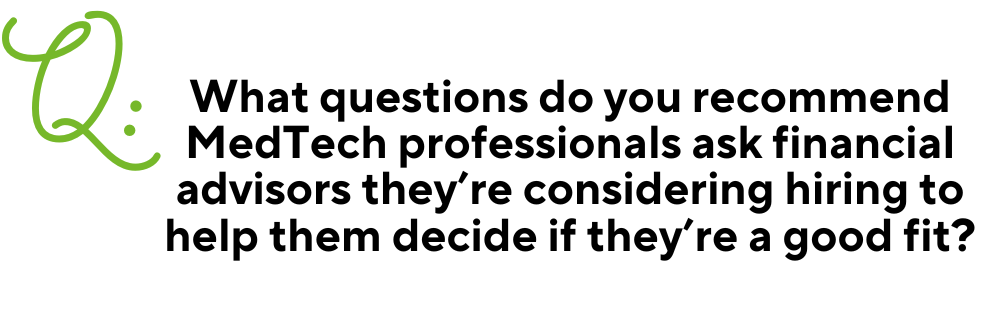

We would encourage MedTech professionals to ask any financial advisor they’re considering hiring the following questions:

- Do you work with many clients that generate significant income from equity compensation plans?

- Do you have any special training in equity compensation planning?

- Do you understand the challenges employees and founders of private company start-ups have that differ from public companies?

- Do your services focus on investments? Or do you coordinate all the financial planning, tax, company benefit, and charitable giving activities I need to consider?

- Are you able to provide guidance with estate planning?

- Is your firm an Independent Registered Investment Advisor with the requirement to act as a fiduciary? Or do you work for an insurance company or broker-dealer that maintains a lower sales suitability standard?

- Will I need to pay separate fees for financial advice and investment advice? Or do you offer an all-inclusive wealth management service?

Answer:

I am often surprised by MedTech professionals’ incredible intelligence and ambition in their field of expertise. And that they are often missing out on many advantages of the benefit options available to them. Such as their benefit plans, tax optimization, and investment portfolio options. The reality is they are incredibly focused on their careers. So, finding the time needed to be effective with personal finances is difficult. That’s where our team can step in and form a functional plan.

Answer:

We worked with a head bio engineer at one of the major device companies in Minneapolis. They planned to exit the company for an opportunity with a local startup. This professional had accumulated years’ worth of stock in the company inside their 401(k) plan. Further, they held a significant number of stock options from incentive plans.

Our team worked with the company’s 401(k) provider to utilize a strategy dealing with NUA (Net Unrealized Accumulation). We were able to save a large sum in future taxes on stock accumulated in the plan for our client. Further, we salvaged as many of the unvested stock options before the professional left. These would have otherwise lost due to time limits imposed in stock option plans post termination.

This planning case was an eye opener to the incredible value we bring to MedTech industry clients. Our team is able to help them make informed decisions with their finances. All while they get to focus on creating breakthrough medical technology.

*Past performance is not a guarantee of future results.

Ready to Take the First Step?

This is a 45-min call to learn about your financial vision & goals and see if we’re a good fit.

Our calls are always relaxed and pressure-free.

Have Questions About Financial Planning for MedTech Professionals?

We have the answers.

Related Posts

-

Looking For a Financial Advisor for MedTech Professionals?

Are you a professional working in the MedTech industry? A financial advisor who understands the unique needs of MedTech careers such as medical device representatives, executives, and founders in this industry can help you make smarter…

10 Min Read

By Matthew Nelson

April 18, 2024 -

7 Expert Strategies to Maximize Your 401(k)

Are you looking to supercharge your retirement savings? Securing your financial future involves smart planning and strategic moves. Especially, when it come to your 401(k). Maximizing your 401(k) is key to a healthy financial future. Here…

4 Min ReadBy Matthew Nelson

April 4, 2024 -

MedTech Industry Benefits & Personal Finances

The world of MedTech is dynamic, with a goal to drive impactful change. Whether you’re a Medical Device Representative, an executive leader, or are forging your path within MedTech, the industry offers unique benefits with financial…

2 Min ReadBy Matthew Nelson

March 21, 2024